Best Apps to Send Money from UAE: What the apps actually charge, which corridors they’re best for, and the hidden exchange-rate cost most people miss.

| Exchange rates and fees fluctuate daily. All figures in this guide are indicative based on current published data. Always check the final rate and total cost inside each app before confirming any transfer. |

For many UAE residents, sending money home is a regular part of life—whether it’s for monthly family support, school fees, or the occasional emergency. While bank transfers are the most familiar route, they often come with hidden costs. A standard transfer can involve a flat fee of AED 25–50, but the real expense is usually tucked away in the exchange rate. For a transfer to India, for example, the spread between a bank’s rate and the real mid-market rate can easily reach 40–50 paise per dirham. Over the course of a year, those small margins add up to AED 1,500 or more in lost value.

The apps in this guide are designed to bypass these traditional hurdles. Instead of relying on the SWIFT network, they leverage local banking partnerships to move money, which cuts out many of the intermediary fees banks charge. When comparing these services, it is helpful to look past the “zero fee” marketing and focus on the exchange rate markup, as that is where the bulk of the cost is usually hidden. A service with a small upfront fee but a competitive rate often proves cheaper than one that claims to be “fee-free” but applies a significant markup.

Below is a breakdown of ten money transfer apps commonly used in the UAE, along with notes on which corridors they serve best. We have highlighted four—Wise, Remitly, Al Ansari Exchange App, and e& money—as reliable options depending on your specific needs.

Related : Top 16 Apps Every Dubai Resident Needs on Their Phone

Quick Comparison

| App | Best for | Transfer fee | Rate markup | Speed |

| Wise | Rate transparency, large transfers | 0.4%–1.5% | 0% (mid-market) | Instant–1 day |

| Remitly | India, Philippines, Pakistan (Express) | AED 0–15 | 0.5%–2% | Minutes–3 days |

| Al Ansari Exchange | UAE bank/cash link, instant transfers | AED 0–25 | Varies by corridor | Instant–1 day |

| e& money | UAE-based super app, wallets | AED 0–15 | Varies | Minutes |

| LuLu Money | India, Bangladesh, Nepal zero-fee | AED 0 | 1.5%–2% | Minutes–1 day |

| Western Union | Cash pickup, unbanked recipients | AED 0–25 | 1%–3% | Minutes–2 days |

| Skrill | Pakistan; tech-savvy senders | None | 3.99%–4.99% | Hours–1 day |

| WorldRemit | Africa, mobile wallets | AED 5–20 | 1%–2.5% | Minutes–2 days |

| Al Fardan Exchange | Gulf corridors, in-branch option | Varies | Competitive | Same day |

| CurrencyFair | UK, Canada, Europe (larger transfers) | €3 flat | 0.45% | 1–3 days |

| Rate markup is the percentage added on top of the mid-market (interbank) rate. Even ‘zero fee’ apps earn their revenue here. On a AED 5,000 transfer, a 2% markup costs AED 100 that never appears as a visible charge. |

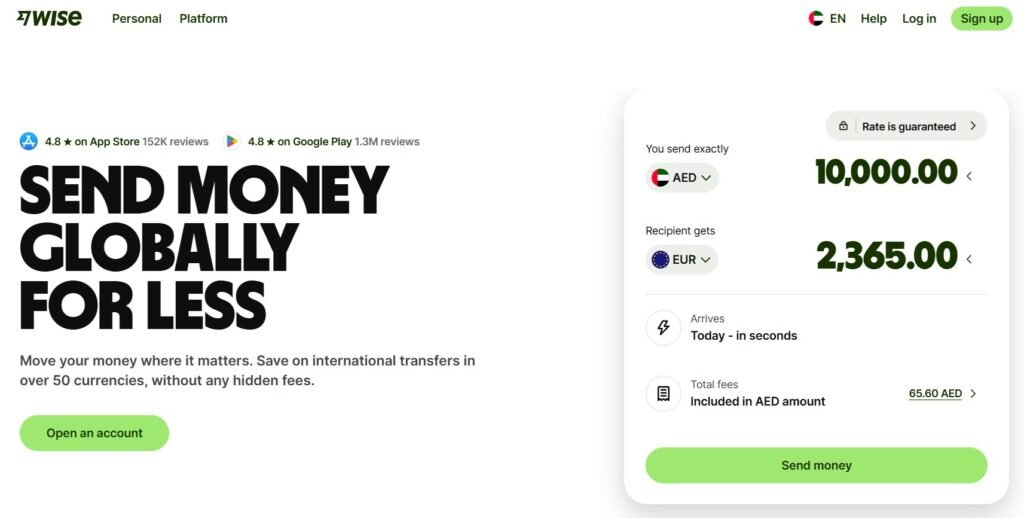

1. Wise

Best for rate transparency and larger transfers

Wise built its reputation on one simple idea: use the real mid-market exchange rate and charge a small, visible fee instead of hiding the cost in a rate markup. That fee typically runs 0.4% to 1.5% depending on the corridor and payment method — low enough that it almost always comes out cheaper than apps that offer ‘zero fees’ but quietly move the rate. A AED 5,000 transfer to India through Wise costs roughly AED 35–60 all in, compared to AED 150–250 through a typical UAE bank. Over 74% of Wise transfers arrive in under 20 seconds on major corridors.

For the UAE, the practical corridors are India (IMPS, NEFT), Philippines (GCash, bank), Pakistan, UK, US, and most of Europe. The Wise account also functions as a multi-currency wallet — you can hold AED, USD, EUR, GBP and send or receive in any of them without converting. Useful if you’re paying overseas invoices or receiving freelance income from abroad. The slight limitations: you fund transfers via linked bank account or card (no cash option), and in rare cases on less-common corridors it’s slower than stated. But for the majority of regular remittances, it’s the benchmark everything else is measured against.

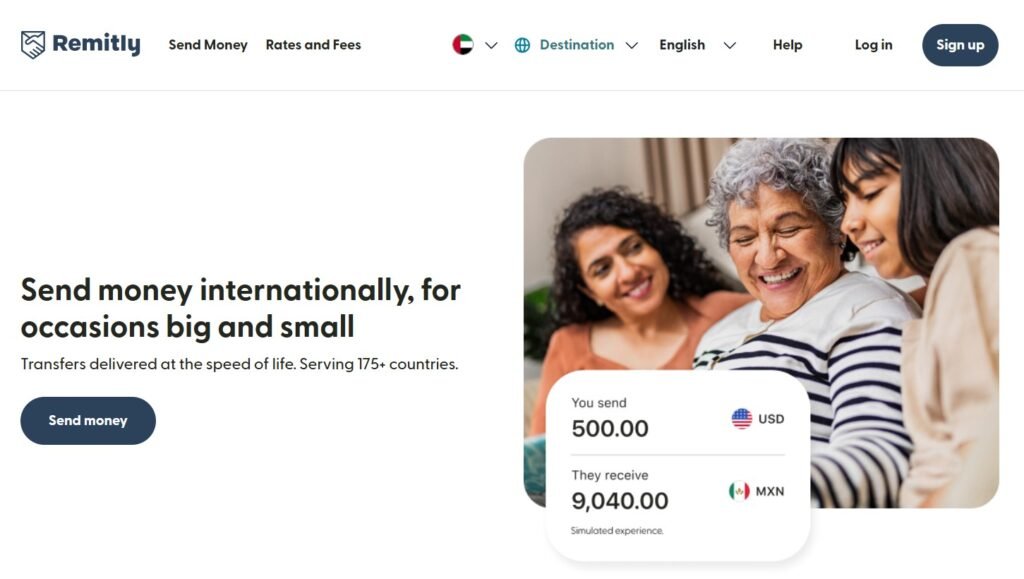

2. Remitly

Best for fast transfers to India, Philippines and Pakistan

Remitly has consistently ranked as the lowest-fee app for UAE-to-India transfers on independent comparison platforms, including coming top for 36.5% of all UAE search queries on Monito’s engine. For Pakistan, it ranks as the top option on 56.2% of searches. That performance is built on tight corridor-specific pricing rather than a universal low-rate model. There are two service tiers per transfer. Economy transfers (funded by bank account) arrive in 1–3 business days at the best rate. Express transfers (funded by debit card) arrive in minutes at a slightly higher rate.

The difference in total cost is usually AED 10–20, which is worth it when sending rent or emergency funds. Remitly covers over 135 countries with multiple payout methods per destination: bank deposit, cash pickup, mobile wallet (GCash in the Philippines, bKash in Bangladesh) and home delivery in some markets. There are no monthly fees, and the first transfer for new users often comes with a promotional rate. One thing to note: Remitly works outbound from the UAE, not inbound. If you need to receive money into a UAE account from abroad, it won’t help there.

3. Al Ansari Exchange App

Best for UAE bank-linked and cash transfers with UAE PASS

Al Ansari Exchange is one of the most widely used exchange houses in the UAE, and its app brings that network into the phone. It connects directly to UAE bank accounts and debit cards — funded transfers are typically processed the same day or faster. Registration uses UAE PASS, the federal digital identity system, which makes onboarding faster than most apps for UAE residents.

The network covers over 50 countries with bank deposit and cash pickup options, and the exchange rates are competitive on major corridors (India, Pakistan, Philippines, Egypt). The app has removed debit card fees through a partnership with Mastercard and Visa, which is a meaningful saving for card-funded transfers.

The physical backup is worth mentioning: with over 200 branches across the UAE, cash transfers and in-person assistance are available when the app isn’t enough — particularly for recipients in countries where reliable banking infrastructure is patchy and cash pickup matters. The app also shows rates in real time before you commit, which removes the ‘rate lock’ uncertainty some exchange houses used to carry.

Rate markup varies by corridor and isn’t always the tightest, but the combination of UAE PASS integration, local familiarity and physical fallback makes it the most practical app for residents who want something deeply embedded in how UAE financial services work.

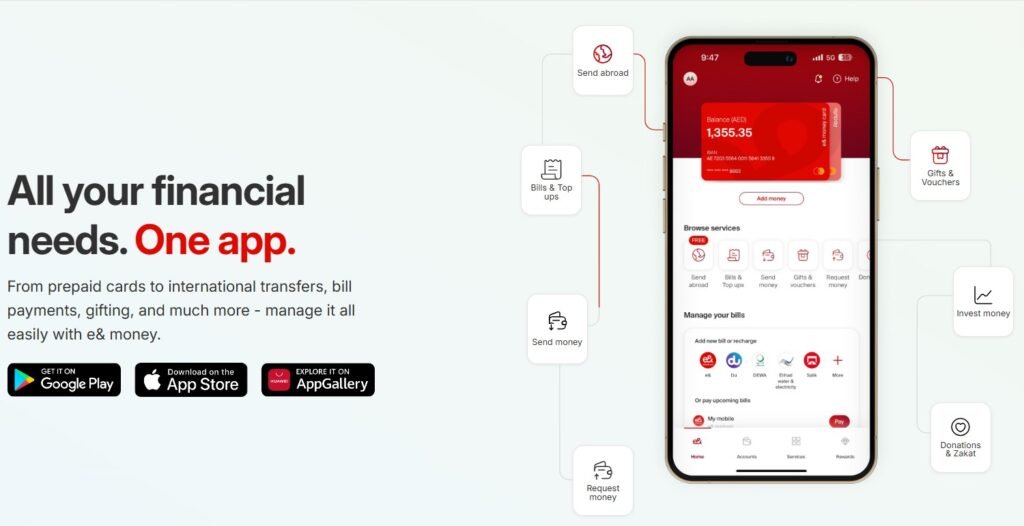

4. e& money

Best UAE-native financial super app for direct global transfers

e& money (formerly Etisalat’s financial arm) is a UAE-licensed digital financial platform that covers money transfers, bill payments, phone top-ups, and peer-to-peer sending within a single app. Transfers go directly to overseas bank accounts, mobile wallets, or are available for cash pickup — the payout options depend on the destination country.

For UAE-based users, e& money has a distinct practical advantage: it integrates with the e& telecom account and UAE PASS, making setup straightforward for the large portion of the population that’s already on the e& network. Transfers can be funded via UAE bank account or card.

The fee structure depends on the destination and transfer size, but it’s competitive for most major corridors in South Asia and the Arab world. The platform is Central Bank UAE-licensed, which matters for anyone who wants local regulatory oversight on their transfers rather than relying solely on an overseas fintech’s licensing. It’s a strong option if you’re already an e& customer and want everything in one place, or if you’re sending to destinations where the app has specific wallet integrations that competitors don’t.

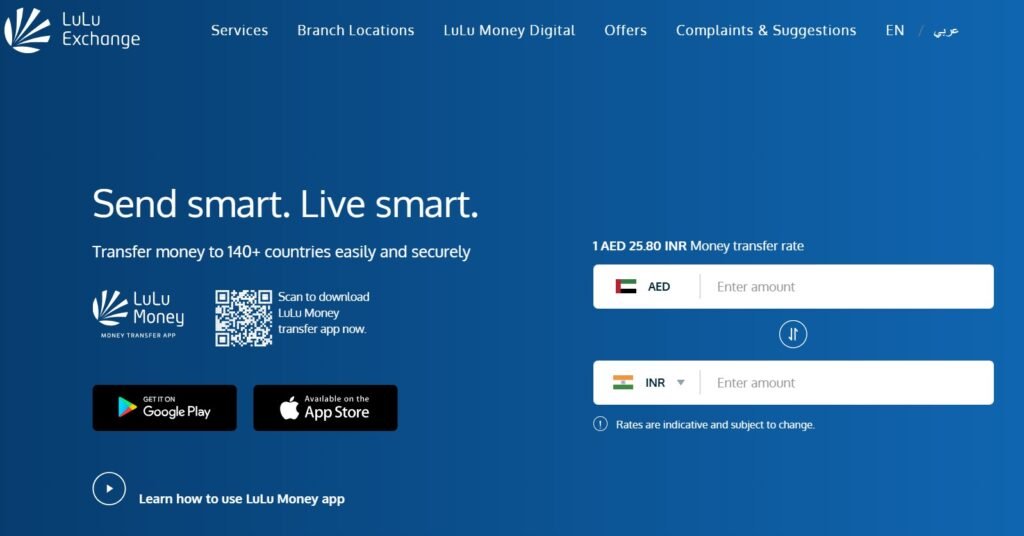

5. LuLu Money

Best for zero-fee transfers to India, Philippines, Bangladesh and more

LuLu Money is the app arm of LuLu International Exchange, which is Central Bank UAE-licensed and has over 145 physical branches across the country. The headline feature is zero transfer fees on selected corridors — India, Philippines, Bangladesh, Nepal, Pakistan, Egypt and Sri Lanka — which makes it genuinely cost-effective for residents sending smaller amounts regularly. The exchange rate markup runs around 1.5–2% above the mid-market rate, which is competitive for a fee-free service.

On a AED 2,000 transfer to India, the effective cost is around AED 30–40 in rate margin, with no flat fee on top. For regular monthly remittances in the AED 500–3,000 range, this often works out cheaper than apps with a small flat fee. The physical branch network is the other practical advantage: if something goes wrong or a recipient needs cash pickup, walking into a LuLu Exchange branch is a real option rather than a support ticket.

The eKYC onboarding is fast, and the app supports transfers to over 170 countries. User reviews flag some delays and rate discrepancies on certain transactions — the app can sometimes show a rate at initiation that differs slightly from the processed rate. Worth checking the confirmation details carefully before sending. → LuLu Money — International Money Transfer

6. Western Union

Best when recipients don’t have a bank account

Western Union’s global network of 500,000+ agent locations is its defining advantage and the reason it remains relevant in 2026 despite being outcompeted on fees by newer apps. If the person receiving money doesn’t have a reliable bank account — whether in rural Philippines, parts of Africa, or smaller towns across South Asia — Western Union cash pickup is often the only option that actually works. For banked recipients, Western Union’s rates are competitive but rarely best-in-class.

Exchange rate markups run 1–3% depending on the corridor, and fees vary by transfer amount, payment method and destination. The rule of thumb: bank-funded transfers are cheaper than card-funded ones, and bank deposit is cheaper than cash pickup. The app is well-designed, transfer tracking is reliable, and the UAE has hundreds of agent locations for in-person sending. For the population of UAE residents sending money to recipients who need cash in hand, nothing else has Western Union’s reach.

7. Skrill

Best for Pakistan transfers; digital wallet power users

Skrill’s strongest card in the UAE context is Pakistan: Monito’s independent data puts Skrill at the lowest fees for 56.2% of UAE-to-Pakistan searches. For that specific corridor, it’s worth comparing directly with Remitly and Wise before deciding. The cost model is unusual: Skrill charges no flat transfer fee when you fund via bank transfer, but earns its revenue entirely through the exchange rate markup, which sits at 3.99–4.99% above the mid-market rate.

That’s higher than most alternatives on this list. On a AED 5,000 transfer, the hidden markup costs roughly AED 200 — more expensive than it looks at first glance. Skrill is also a full digital wallet: you can hold multiple currencies, pay at online retailers that accept Skrill (particularly useful for freelancers and online businesses), and get a prepaid Mastercard for physical spending. For users who want the wallet functionality alongside remittances, the package makes more sense than using it purely as a transfer tool. No cash pickup option.

8. WorldRemit

Best for Africa, mobile wallets and airtime top-ups

WorldRemit covers over 130 countries with a particularly strong network in Africa and Southeast Asia. Mobile money wallet delivery — M-Pesa in Kenya, MTN Mobile Money in Ghana, GCash in the Philippines, bKash in Bangladesh — is where it stands out against apps that only offer bank deposits.

Fees run AED 5–20 depending on destination and transfer size, with a rate markup of 1–2.5%. For recipients in countries where mobile wallets are the primary financial tool rather than bank accounts, WorldRemit’s delivery options are genuinely broader than most alternatives. Airtime top-ups to foreign numbers are also available directly from the app. For UAE residents sending money to East or West Africa, or to Southeast Asian recipients who use mobile wallets rather than banks, it’s the strongest option on the list. → WorldRemit — Send Money Online

9. Al Fardan Exchange

Best for Gulf corridors and high-value transfers with branch support

Al Fardan Exchange is a UAE-founded, Central Bank-licensed exchange house with a strong presence in Dubai and Abu Dhabi. Its digital app handles international transfers and currency exchange, with competitive rates on Gulf and South Asian corridors. The exchange rates are generally tight, and the service works well for larger transfers where having a licensed UAE entity with physical locations provides reassurance.

Al Fardan handles corporate and personal transfers, and the branch network makes it a credible option for residents who want the option of in-person assistance for larger or more complex transactions. Less widely discussed than LuLu or Al Ansari in digital circles, but worth comparing rates directly for corridors where exchange houses traditionally have better rates than fintech apps.

10. CurrencyFair

Best for UK, Canada and Europe transfers with a peer-matching model

CurrencyFair uses a peer-to-peer exchange model that, for certain corridors, produces rates very close to the mid-market rate. It ranked as the cheapest option for 36.3% of UAE-to-Canada searches on Monito’s engine, making it the standout choice for Canadian dollar transfers specifically.

The flat fee per transfer is low (around €3 equivalent) and the exchange rate margin is typically just 0.45%, making it genuinely competitive for anyone sending to the UK, EU countries or Canada. The tradeoff is that it’s less useful for the high-volume corridors (India, Pakistan, Philippines) where Remitly and Wise have more optimised networks.

The app and platform are well-designed, and the peer-matching model means rates can actually be better than standard provider rates if your transfer matches a counterparty. Setup is straightforward and KYC is fully online.

How to Actually Compare Before You Send

The fastest way to compare on any specific transfer is to use a live comparison tool. Remit.ae and Monito both pull real-time rates from most of the apps above for AED corridors and show the total cost including both fees and rate markup before you commit to any one provider. Run your transfer amount and destination through either site before using any single app, particularly for transfers over AED 2,000 where the rate difference between providers adds up quickly.

A few things to check inside whichever app you choose:

- The rate shown at the start versus the rate locked at confirmation — some apps update rates between those two screens

- The delivery method: bank deposit and mobile wallet usually carry lower fees than cash pickup on the same app

- The funding method: bank transfer is typically cheaper than card funding by 1–2%, and most apps pass that saving on

- Transfer limits: some apps cap per-transaction or daily amounts, which matters for larger or urgent transfers

For most UAE residents sending money to South Asia or Southeast Asia regularly, the practical short answer is: Wise if you prioritise the best rate, Remitly if you need money there in minutes, Al Ansari if you want a UAE-native app with physical backup, and LuLu Money if you’re doing frequent smaller transfers to the zero-fee corridors.

The Bottom Line

A UAE bank will handle international transfers, but paying AED 150–200 in hidden rate markup per transaction when you could pay AED 30–60 is a significant difference across a year of regular remittances. The ten apps in this guide are all Central Bank UAE-licensed or operate through licensed partners, all process transfers legally and safely, and all offer better value on most corridors than a standard bank wire.

Check the rate on Remit.ae or Monito before your next transfer, compare two or three of the options above, and the savings tend to become obvious within the first transaction.