Dubai’s free zones have long been the path of least resistance for foreign entrepreneurs wanting a foothold in the Middle East — and that path is better-paved than ever. Fully digital approval workflows, a clearer corporate tax framework, and a freezone landscape now spanning over 30 designated zones across the emirate mean there are more options, more flexibility, and, frankly, more to get right from the start.

The basics haven’t changed. You still get 100% foreign ownership, zero personal income tax, full profit repatriation, and a business environment that genuinely prioritises speed. What has changed is the detail — especially around corporate tax, QFZP (Qualifying Free Zone Person) compliance, and which zones offer the best fit for which type of business.

This guide walks through every stage of the process, from choosing your free zone to receiving your trade licence and opening a corporate bank account. No guesswork.

Step by Step :How to Set Up a Business in Dubai Freezone

Setting up a business in a Dubai Free Zone is one of the most strategic moves an entrepreneur can make, offering a streamlined pathway to 100% foreign ownership and unparalleled tax efficiencies. While the process is designed to be business-friendly, navigating the specific requirements of your chosen jurisdiction requires a clear, structured approach.

Here is the exact step-by-step framework to transition your business from a blueprint to a fully operational entity.

What Is a Dubai Free Zone, and Why Does It Matter?

A free zone is a legally designated economic area operating under its own regulatory authority, separate from Dubai’s mainland commercial framework governed by the Department of Economy and Tourism. Each zone has its own licensing rules, visa allocations, office requirements, and fee structure.

That separation is the whole point. Companies registered in a free zone are not considered ‘onshore’ businesses for certain regulatory purposes, which historically meant different tax treatment, customs exemptions on goods moving in and out of the zone, and no requirement for a local UAE national sponsor.

For most foreign founders , the core appeal comes down to four things:

- 100% foreign ownership — no need for a UAE national partner or sponsor in any free zone

- Tax efficiency — eligible businesses can access a 0% corporate tax rate on qualifying income under the QFZP regime

- Speed — most free zone licences are issued within 3 to 10 business days, significantly faster than mainland processes

- Operational flexibility — flexi-desks, shared offices, and virtual address packages reduce overhead significantly for early-stage businesses

One important clarification : free zones are not automatically tax-free. The UAE introduced corporate tax in June 2023, and free zone companies now need to actively qualify for the 0% rate. More on that shortly.

Step 1: Choose the Right Free Zone

This is the most consequential decision in the whole process, and the one most people rush. Dubai alone has over 30 free zones , each built around specific industries and business models. Picking the wrong one doesn’t necessarily end your company, but it can make banking harder, limit your visa quota, or leave you paying for infrastructure you don’t need.

Here’s how the major zones break down for different business profiles:

DMCC (Dubai Multi Commodities Centre)

The world’s largest free zone by registered companies, DMCC hosts over 24,000 businesses from 180 countries . Located in Jumeirah Lakes Towers, it’s the go-to choice for commodities traders, consulting firms, and companies that want premium banking relationships out of the gate. Starting licence fees are in the mid-tier range — broadly AED 25,000 to AED 35,000+ depending on package — and it requires AED 50,000 in paid-up share capital. If institutional credibility matters to your pitch or your bank, DMCC is often worth the extra cost.

IFZA (International Free Zone Authority)

For solo founders, digital businesses, and startups watching their cash flow, IFZA is consistently the most popular entry point in Dubai. Licences start from around AED 12,200 to 12,900, there is no minimum share capital, setup is fully digital, and incorporations typically complete in three to five business days. Banking is broadly accepted, though IFZA companies sometimes face more conservative scrutiny from tier-one UAE banks than DMCC entities.

DIFC (Dubai International Financial Centre)

If you’re in financial services — asset management, private equity, family office structuring, fintech, or banking — DIFC is the only serious option. It operates under English common law with its own regulator (the DFSA), which is a major draw for international investors who need familiar, enforceable governance. Starting licences run AED 50,000 and above, making it the most expensive zone in Dubai. The premium reflects the ecosystem: DIFC houses over 5,000 companies including global banks, hedge funds, and leading fintech firms.

JAFZA (Jebel Ali Free Zone)

Established in 1985, JAFZA is the region’s largest industrial free zone and sits adjacent to Jebel Ali Port — the world’s ninth-largest container port. If your business is import/export, warehousing, manufacturing, or logistics at any meaningful scale, JAFZA’s physical infrastructure and designated-zone VAT treatment for goods are genuinely valuable. It’s not the place for a digital consultancy.

Meydan Free Zone

Meydan has become a popular choice for remote-first founders and e-commerce operators who want a central Dubai address without DMCC pricing. Costs are comparable to IFZA, the setup is streamlined, and it suits service businesses, online operations, and consulting firms well. Banking acceptance is broadly similar to IFZA.

Dubai Silicon Oasis (DSO / DTEC)

Tech startups wanting an on-the-ground ecosystem rather than just a licence address tend to gravitate toward DSO. The DTEC hub within DSO offers co-working, accelerator programmes, and access to venture networks. Good for early-stage founders who want community alongside compliance.

💡 Quick decision rule : Start with your business activity. Fintech or financial services → DIFC. Trading, commodities, or premium credibility → DMCC. Consulting, digital services, or startup on a budget → IFZA or Meydan. Logistics, manufacturing, or import/export at scale → JAFZA.

Step 2: Define Your Business Activity and Licence Type

Every free zone maintains an approved list of business activities, and the activity you select determines your licence type, the facilities you need, and — critically for tax purposes — whether your income qualifies as ‘qualifying income’ under the QFZP framework.

The four standard licence types are:

- Professional / Service Licence — for consulting, IT, marketing, legal advisory, and similar service businesses. Typically the most affordable licence category.

- Trading / Commercial Licence — for businesses buying and selling goods. Often requires a flexi-desk at minimum and may require a warehouse if goods are physically stored.

- Industrial / Manufacturing Licence — for production and manufacturing operations. Usually requires dedicated warehouse or factory space within the zone.

- Freelance Permit — for individual professionals in sectors like media, technology, design, and education. Allows you to operate as a sole practitioner without forming a full company.

Be precise when selecting your activity. Vague descriptions can delay approval, complicate banking, and create ambiguity in your tax position. If you plan to do consulting and training, list both. If you’ll trade physical goods alongside a service offering, you may need a combined or dual licence — some zones permit this, others require separate entities.

⚠️ Tax note: The activities permitted under your licence directly affect whether your income qualifies for the 0% corporate tax rate. Selecting a broad or inaccurate activity can jeopardise your QFZP status later. Get this right before you file.

Step 3: Select Your Legal Structure

Most free zone businesses operate as one of two structures: a Free Zone Establishment (FZE) for a single shareholder, or a Free Zone Company (FZC / FZCO) for two or more shareholders. Both offer limited liability. The choice is straightforward — if you’re the sole owner, go FZE; if you have co-founders or investors, go FZC.

Foreign companies expanding into Dubai can also register as a Free Zone Branch, which keeps the parent company’s name and legal identity but avoids creating a new standalone entity. This is common for multinationals testing the UAE market before committing to a fully independent subsidiary.

Share capital requirements vary significantly by zone. Most — including IFZA, Meydan, Dubai Media City, and Dubai Internet City — have no minimum share capital requirement, which significantly reduces the upfront cash burden. DMCC requires AED 50,000. DIFC has its own requirements for regulated entities that can be substantially higher.

Step 4: Reserve Your Trade Name

Your company name must be approved by the free zone authority before registration proceeds. UAE naming rules apply across all zones — names cannot be offensive, reference religious or political figures, or duplicate existing registered names. Acronyms and abbreviations require explanation.

Most zones handle name reservation digitally through their business portal, and it’s usually resolved within one to two business days. Have two or three options ready in case your first choice is taken. Once approved, the name reservation is typically valid for a set period (commonly 30 to 60 days) during which you must complete your application.

Step 5: Prepare and Submit Your Documents

Document requirements are fairly consistent across zones, though some add sector-specific items. The standard checklist for an individual founding a new company looks like this:

- Passport copy (all shareholders and directors)

- Passport-sized photographs

- Proof of residential address — utility bill or bank statement, usually dated within three months

- Completed application form (zone-specific, usually available online)

- Business plan — required by some zones, particularly for regulated activities; not always mandatory for straightforward service or trading licences

- No-objection letter (NOC) — required if the applicant is currently employed in the UAE on a sponsored visa

- KYC (Know Your Customer) forms — standard compliance documentation required by all zones

If you’re setting up a branch of an existing company rather than a new entity, expect to also provide: the parent company’s Certificate of Incorporation, Memorandum and Articles of Association, a board resolution authorising the branch, and the parent’s audited financial statements.

All documents originally in a language other than English or Arabic typically require certified translation. Attestation requirements vary — some zones require apostille for foreign documents, others accept notarised copies. Confirm requirements with your chosen zone before preparing documents.

📋 Tip: Prepare documents in advance and ensure they’re current. Many founders lose days to expired proof-of-address documents or signatures that don’t match passport copies exactly. Small details cause real delays.

Related : The Top Guide to Buying vs. Renting in Dubai

Step 6: Secure Your Office Space

Every free zone requires a registered business address. But ‘office’ covers a wide spectrum, from a fully serviced dedicated unit to a flexi-desk in a shared workspace to what’s sometimes called a virtual or smart office — essentially a registered address with mail handling and meeting room access on a pay-per-use basis.

The three main options and what they actually mean:

- Flexi-Desk — a non-dedicated workspace in a shared environment, often included in entry-level licence packages. Sufficient for service businesses with no physical operations. This is the cheapest route and works well for remote-first companies.

- Serviced Office — a dedicated private office within the free zone’s managed facilities. Comes with a higher annual cost but improves your banking narrative and supports more visa allocations.

- Warehouse / Industrial Unit — for businesses that physically handle, store, or manufacture goods. Required for trading licences involving goods in many zones. Costed separately and significantly more expensive.

One thing worth understanding: your office type directly influences your visa quota. Flexi-desk packages often include entitlement for one or two investor visas. Moving to a serviced office typically increases that allocation. If you plan to bring employees into the UAE under your free zone licence, your office footprint needs to support that.

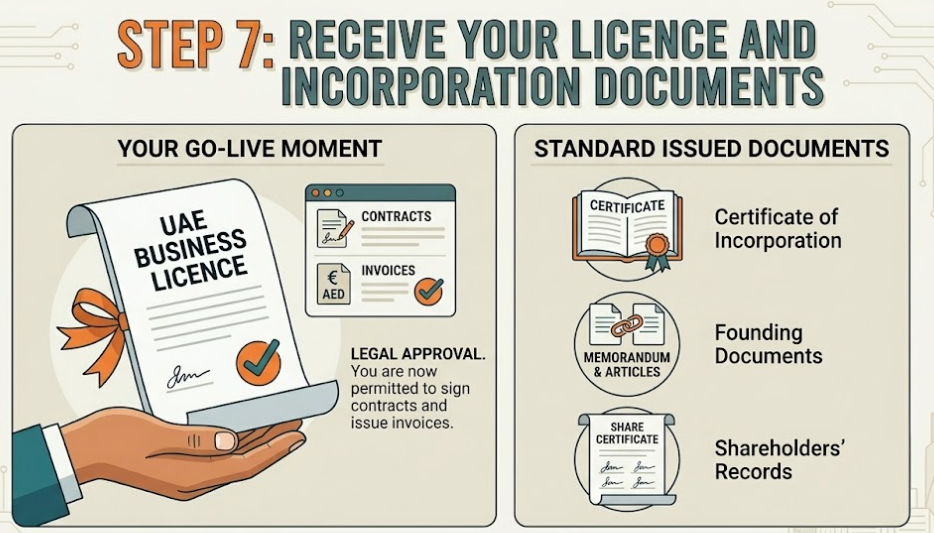

Step 7: Receive Your Licence and Incorporation Documents

Once your application is approved and fees are paid, the free zone authority issues your trade licence and incorporation documents. This is the legal ‘go-live’ moment for your company — the point at which you can sign contracts, issue invoices, and begin the next steps of visa processing and banking.

Standard documents issued at this stage include: the trade licence itself, the Certificate of Incorporation, the Memorandum and Articles of Association (or equivalent founding documents), and share certificates if applicable.

Timeline, realistically:

- IFZA, Meydan, SHAMS: 3 to 5 business days for licence-only setups

- DMCC, DSO, DHCC: 5 to 10 business days

- DIFC: 7 to 14 business days due to tighter regulatory KYC requirements

These timelines assume clean documentation. Missing information, incomplete KYC, or activity approvals required from an additional UAE authority (common in health, food, and education sectors) can add days or weeks.

Step 8: Apply for UAE Residency Visas

The investor visa is what turns your free zone licence into a genuine UAE residency — and for many founders, this is the primary personal goal alongside the business setup. A UAE residence visa under your free zone company gives you the right to live in the UAE, open a personal bank account, lease an apartment, obtain an Emirates ID, and sponsor family members.

The visa process involves:

- Entry permit — issued first, allows you to enter the UAE for medical testing and biometric registration

- Medical fitness test — blood test and chest X-ray, conducted at approved health centres

- Emirates ID registration — biometric data captured at an ICA service centre

- Visa stamping — the actual residency stamp placed in your passport

End-to-end, the visa process typically takes two to four weeks from when the entry permit is issued. The number of visas your company can support depends on the size of your office package — a standard flexi-desk usually covers one or two investors, while larger office spaces unlock more allocations for employees and dependents.

Family visas (for spouses and children) and domestic worker visas can be sponsored once your own investor visa is confirmed. Your Emirates ID must be issued before you can open a personal bank account in the UAE.

Step 9: Understand the Corporate Tax Position

This section matters more than it did two years ago. The UAE introduced corporate tax (CT) from 1 June 2023, and while free zones retain significant advantages, the ‘tax-free zone’ shorthand that circulated for decades needs updating.

The current structure :

- Standard CT rate: 9% on taxable profits above AED 375,000 (approximately USD 102,000)

- 0% rate on qualifying income: available to businesses holding Qualifying Free Zone Person (QFZP) status

- Small Business Relief: companies with annual revenue at or below AED 3 million can elect for full CT relief through the end of December 2026

QFZP status is not automatic. To qualify, your free zone company must:

- Be a juridical person registered in a free zone

- Maintain adequate economic substance in the UAE — real staff, genuine operating expenditure, and management decisions taken in the UAE, not just a registered address

- Earn income primarily from qualifying activities — broadly, transactions with other free zone entities and overseas clients

- Pass the de minimis test: non-qualifying income must not exceed 5% of total revenue or AED 5 million, whichever is lower

- Have audited financial statements

- Comply with transfer pricing rules and documentation requirements

The stakes are high if you miss the mark. A company that fails any single QFZP condition loses the 0% rate entirely — not just on the non-qualifying income stream — and becomes subject to 9% CT on all its income for the current tax year and the four subsequent years.

An important 2025 update: the operative regulation governing qualifying activities is now Ministerial Decision No. 229 of 2025 (issued August 2025), which replaced and repealed MD 265 of 2023. Any QFZP guidance written before September 2025 should be treated as potentially outdated on the specifics of qualifying activities.

⚠️ Important: Talk to a UAE corporate tax adviser before setting up if tax efficiency is a core reason for your free zone structure. The QFZP framework is precise and demands active maintenance — getting it right from day one is far cheaper than fixing it later.

Step 10: Open a Corporate Bank Account

This is consistently where founders encounter the most friction. UAE banks have tightened KYC and AML requirements substantially over the past several years, and free zone companies — especially those with non-resident shareholders or complex ownership structures — can face conservative scrutiny.

A few things that shape how your banking application goes:

- Free zone choice matters: DMCC companies are generally perceived by tier-one UAE banks as higher credibility than IFZA or Meydan entities, even if the underlying business is identical. The zone’s reputation affects the banker’s willingness to onboard quickly.

- Activity clarity is essential: banks want to understand exactly what your company does and how money flows. Trading companies usually need supplier agreements; service companies need client contracts or engagement letters. The clearer and more concrete your documentation, the smoother the approval.

- Traditional banks vs. EMIs: traditional UAE banks (Emirates NBD, Abu Dhabi Commercial Bank, Mashreq, etc.) offer stronger local banking but slower onboarding and higher minimum balance expectations. Electronic Money Institutions (EMIs) like Wise Business, Airwallex, or Wio are significantly faster to onboard and often more multi-currency capable — but they’re not full banks.

Realistic banking timeline: two to four weeks for straightforward cases with clean documentation, potentially longer for complex structures or activities in regulated or sensitive sectors.

One tactical point: open your bank account as soon as your licence is issued. Don’t wait. Banking can take longer than the entire company formation process, and you need the account live before you can meaningfully operate.

What Does It Actually Cost? A Budget Breakdown

Honest cost planning requires looking at total first-year spend, not just the headline licence fee. Here’s a realistic breakdown across different setups:

Budget / Lean Setup (e.g., IFZA or Meydan, service licence, 1 visa)

- Trade licence: AED 12,200 to 13,000

- Flexi-desk (often bundled): AED 0 to 3,000 additional

- Investor visa: AED 3,500 to 5,000 (medical, Emirates ID, stamping)

- Registration fees and admin: AED 1,000 to 2,500

- First-year total: AED 18,000 to 25,000 (approximately USD 4,900 to USD 6,800)

Mid-Tier Setup (e.g., DMCC, trading or service licence, 1–2 visas)

- Trade licence: AED 25,000 to 35,000+

- Shared office / flexi-desk: AED 5,000 to 10,000

- Share capital (DMCC): AED 50,000 (held in company account)

- Visas (×2): AED 7,000 to 10,000

- First-year total: AED 40,000 to 60,000+ (approximately USD 10,900 to USD 16,300+)

Premium Setup (e.g., DIFC, financial services)

DIFC licences start at AED 50,000 and can run significantly higher depending on regulated activity type. Factor in legal and compliance costs, audited accounts, and regulated entity requirements. Total first-year spend of AED 100,000 to AED 200,000+ is not unusual for a regulated DIFC entity.

💰 Hidden costs to plan for: Government registration and knowledge fees (added on top of licence costs), activity approval fees for regulated sectors (AED 500 to 3,000), PRO service fees if using a setup agent, VAT registration if turnover exceeds AED 375,000, and annual corporate tax filing once the Small Business Relief period ends.

Common Mistakes to Avoid

The mistakes that cause the most pain are rarely exotic. They’re structural and preventable.

- Choosing a free zone based on price alone. A cheap licence that creates banking problems costs far more in lost time and missed opportunities than a slightly more expensive zone with better banker relationships.

- Selecting a vague or inaccurate business activity. This causes delays at the licensing stage and can jeopardise QFZP status and banking approval later.

- Ignoring the corporate tax framework. Many founders set up a free zone company assuming automatic tax exemption. The QFZP regime has real substance requirements. Ignoring them until your first FTA filing is expensive.

- Not planning for banking before launch. The most common post-setup complaint from founders is that banking took much longer than expected. Start early, prepare thoroughly, and have a backup option (an EMI) ready while your primary bank account is processed.

- Underestimating renewal costs. Your licence, visa, and office contract all need annual renewal. Budget for year two as carefully as year one — renewal fees are typically similar to initial costs.

Freezone vs. Mainland: When the Freezone Is Not the Right Answer

A free zone structure has genuine trade-offs, and they’re worth knowing before you commit.

The biggest limitation: free zone companies cannot directly sell to customers on the UAE mainland without either working through a mainland registered agent/distributor or obtaining a separate mainland licence. If your primary market is UAE consumers or mainland businesses, a free zone company creates structural friction — legally you need a different entity or a commercial arrangement to bridge the gap.

Mainland companies can operate anywhere in the UAE without restriction, and since 2021 reforms, most mainland activities also allow 100% foreign ownership without a local sponsor. If you plan to open retail premises in Dubai, tender for government contracts, or sell directly to a wide UAE consumer base from day one, mainland may actually be the simpler structure.

The two are not mutually exclusive. Some businesses operate a mainland entity for UAE sales alongside a free zone company for international operations. This is legal and relatively common, but adds administrative overhead.

Getting It Right

Setting up in a Dubai free zone is genuinely accessible — the process is faster, more digital, and more foreigner-friendly than it’s ever been. But ‘accessible’ doesn’t mean ‘automatic’, and the details matter more than ever given the corporate tax framework that now sits underneath all of it.

The businesses that set up cleanly and operate smoothly share a few common traits: they spent time choosing the right zone for their specific activity, they were precise about their business description from the start, they understood the QFZP requirements before they needed to comply with them, and they treated banking as a parallel process rather than an afterthought.

Do those things, plan your budget realistically, and the UAE free zone model is as compelling as its reputation suggests — a legitimate, well-regulated base for an international business, with tax advantages available to those who earn them properly.

Sources & Further Reading

- UAE Federal Tax Authority tax.gov.ae

- DMCC (Dubai Multi Commodities Centre): dmcc.ae

- IFZA (International Free Zone Authority): ifza.com

- DIFC (Dubai International Financial Centre): difc.ae

Disclaimer: This article reflects publicly available information and is for general informational purposes only. It does not constitute legal, tax, or regulatory advice. Costs, rules, and requirements change — always verify with the relevant free zone authority and consult a licensed UAE adviser before making business decisions.