Tips to Cut Expenses in Dubai: No generic budgeting advice. Just the things people who live here have actually made work.

Dubai has a way of separating you from your money faster than almost anywhere else. Not because everything is expensive — it’s genuinely cheaper than London or New York in many ways — but because the city runs on lifestyle peer pressure. Brunches, beach clubs, weekend getaways, a newer car because your colleagues have one. Before you know it, a decent salary disappears without much to show for it.

The tips below are pulled from real conversations — the kind people have on Reddit at 11pm when they’re trying to figure out why their account is empty three weeks into the month. No theory. No motivational fluff. Just things that people living in Dubai have actually found useful.

Tips to Cut Expenses in Dubai

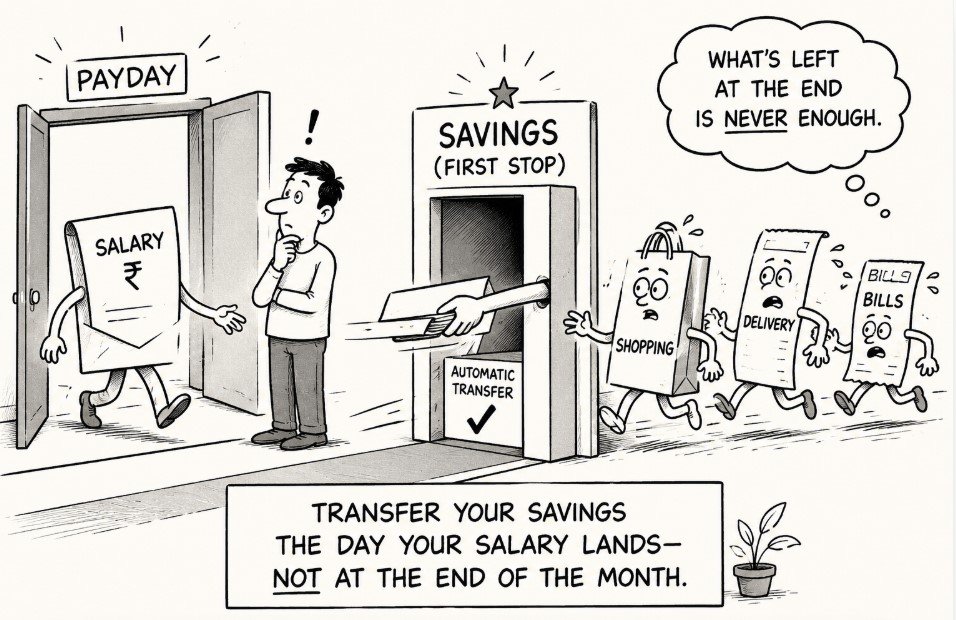

1. Transfer your savings the day your salary lands — not at the end of the month

This is the single most repeated piece of advice from people who’ve cracked saving in Dubai, and it’s repeated because it works. The moment your salary hits, move a fixed amount into a separate account before you touch anything else. Treat it exactly like rent — non-negotiable, not available to spend.

The ‘save what’s left’ approach almost never works here. Dubai eats whatever is loose. There is always something — a dinner, a last-minute trip, a random expense — that takes the last of the month. If saving is the first thing that happens, there’s nothing for lifestyle creep to eat.

2. Open a separate savings account and stop looking at it

The out-of-sight principle genuinely matters. People who keep savings in the same account as their spending almost always dip into it. Open a dedicated savings account and don’t add it to your main banking app’s dashboard if you can avoid it.

WIO Bank and Mashreq both offer savings accounts with competitive interest rates for UAE residents — well above the near-zero rates on standard current accounts. The money sits there, earns a return and, crucially, you don’t scroll past it every morning and start thinking of it as spendable. It’s still accessible for a real emergency, but out of the daily mental picture.

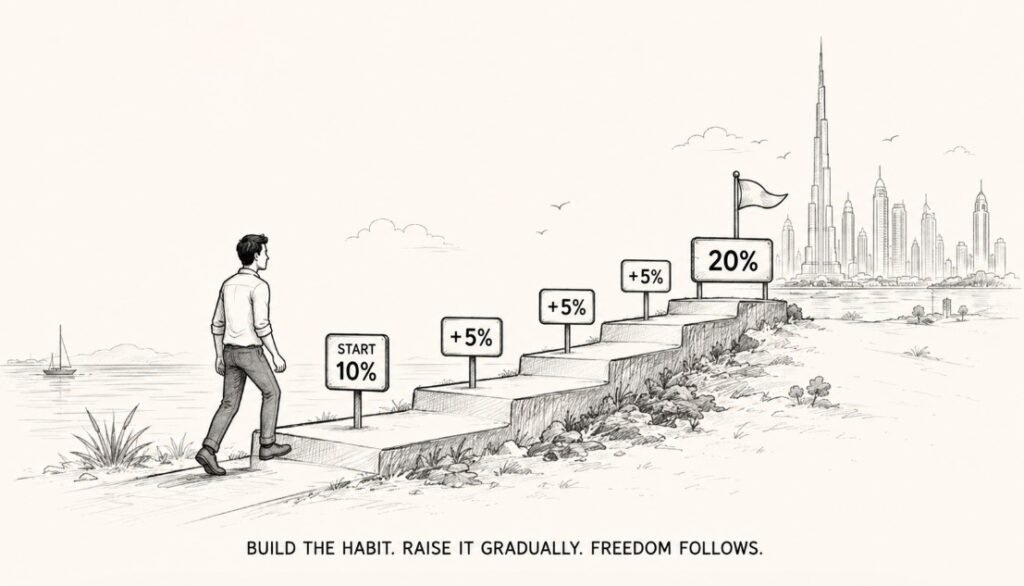

3. Start with whatever percentage you can, then increase it

It is easy to get discouraged from saving when you feel like you have to hit those big, ambitious targets you see in financial advice articles. The reality is that the specific percentage matters far less than the consistency of the habit itself. When you are just starting out, prioritize building the routine over the absolute amount.

A highly effective strategy is to begin with a small, comfortable percentage and commit to increasing it incrementally whenever your income grows. By tying these bumps to your salary raises, you allow your savings rate to climb steadily without ever feeling a sudden or painful pinch in your daily lifestyle. Ultimately, the most successful approach to wealth building is to change the order of operations: treat your savings as your most important fixed expense, and learn to live on what is left afterward, rather than waiting to see what is left over at the end of the month.

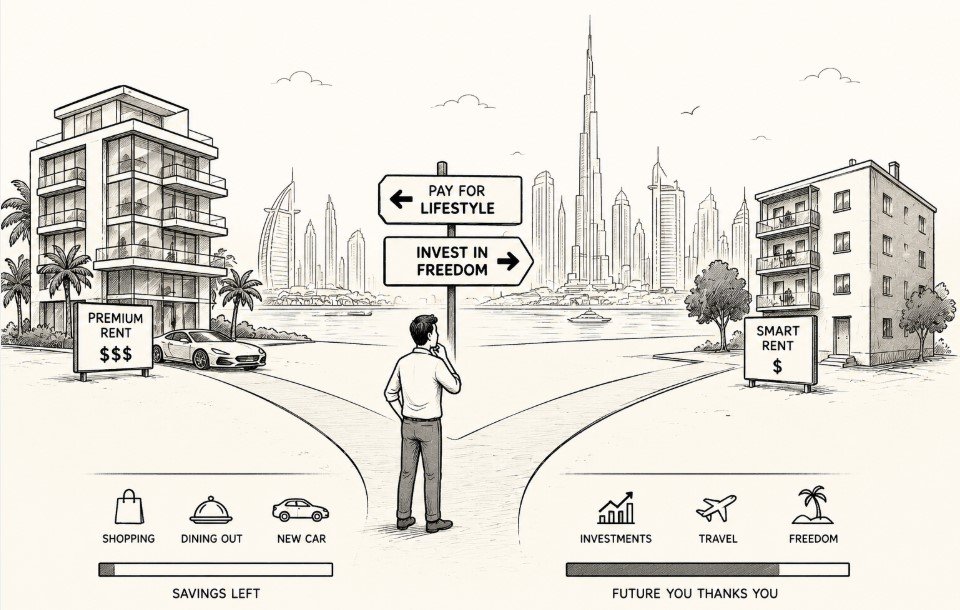

4. Treat your rent choice as a financial decision, not a lifestyle one

Housing is the largest fixed cost for most people in Dubai, and it is the easiest place to unknowingly leak wealth. Paying a premium for a high-profile postcode or a brand-new building often costs tens of thousands of dirhams annually for nothing more than optics. That extra capital, if invested instead of spent on rent, carries significant long-term opportunity cost.

The smarter approach is to prioritize value over trendiness. Established, older communities often provide more square footage and reliable maintenance at a fraction of the cost. While you might trade some convenience in commute time, the resulting increase in your monthly surplus is immediate and tangible. Most financially successful residents in the city treat their first few apartments as a temporary launchpad—living modestly to build a capital base before choosing to upgrade their lifestyle later.

5. Factor DEWA into your apartment choice, not just rent

Most people look at the rent figure and sign. Few people think about what the DEWA bill will look like in that apartment in July and August. Bigger apartments, older buildings with poor insulation, and apartments that face west and take the afternoon sun all produce significantly higher electricity bills during summer.

A smaller, well-insulated apartment might cost slightly more in rent but save you AED 400 to 800 a month on DEWA across peak summer months. Over a full year that’s real money. Before you sign a lease, ask the landlord or building manager what the typical summer DEWA bills run to. Most will tell you honestly.

6. Cook at home. Seriously, just cook at home

This sounds obvious but the numbers are stark. A simple home-cooked dinner for two people costs AED 20 to 30 in ingredients. The equivalent at a casual restaurant is AED 120 to 200. Do that five times a week across a month and the gap is AED 1,500 to 2,000 — every single month, year after year.

Dubai has some of the best supermarkets in the world at reasonable prices. LuLu, Carrefour, and the discount chains like Viva offer solid-quality groceries well below the premium supermarkets. The barrier to cooking at home in Dubai is usually habit and the sheer convenience of delivery, not cost or access. Making it harder to order delivery — deleting the app, switching off notifications — is surprisingly effective.

7. Delivery apps are a slow drain — be specific about how often you use them

Food delivery in Dubai is very good and very fast. It’s also one of the most consistent ways people overspend without noticing. A casual Talabat or Deliveroo order feels small — AED 60 here, AED 80 there — but three or four times a week adds up to AED 800 to 1,200 a month on food that’s usually less satisfying than something cooked fresh.

Setting a hard limit — one or two deliveries per week, or only on Friday nights — rather than a vague intention to ‘cut down’ is the version that actually holds. Some people delete the apps entirely for a month and are surprised by how little they miss them after the first week.

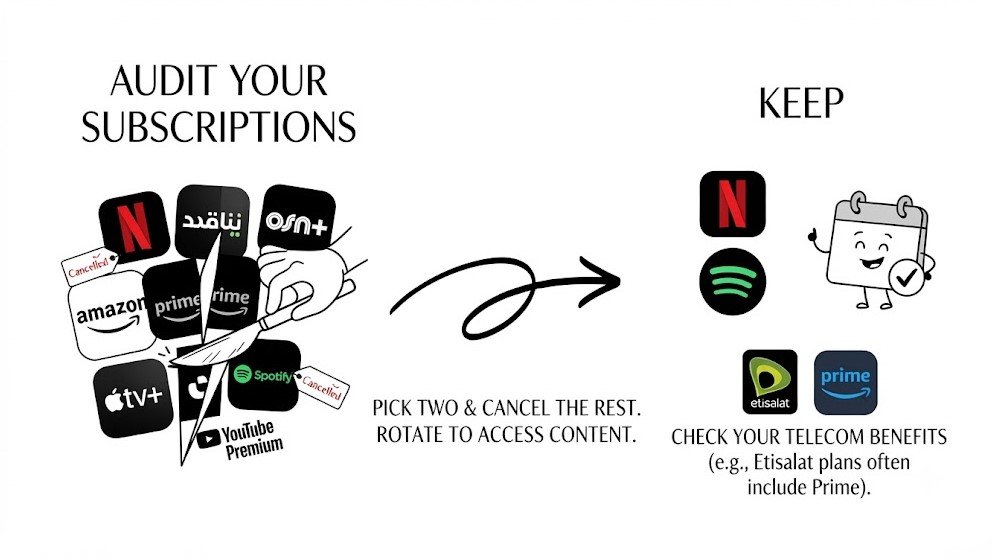

8. Audit your subscriptions every few months

Most people in Dubai are paying for three to five streaming and digital services they use inconsistently. Netflix, Shahid, OSN+, Amazon Prime, Apple TV+, Spotify, YouTube Premium — individually each is cheap, but AED 30 to 60 each adds up quickly.

Pick the two you actually use and cancel the rest. Rotate them every couple of months if there’s specific content you want. One practical tip: switching your Etisalat plan to certain packages includes Amazon Prime at no extra cost. It’s worth checking your telecom benefits before paying separately for services you might already have access to.

9. Use a cashback credit card — but pay it weekly, not monthly

A good cashback credit card used on everyday spending earns you real money back over a year. WIO gives cashback across all expenditure. Several UAE bank cards give 2 to 5 percent back on specific categories like supermarkets, petrol and dining.

The critical discipline: pay the balance every week, not just before the statement deadline. Weekly payment keeps the balance small and visible, removes the temptation to treat the card limit as available funds, and builds a healthy financial habit that most people who’ve tried it say makes a noticeable difference to how they think about spending. A credit card is not extra money. It’s a tool for earning cashback on money you were going to spend anyway.

10. Budget for your big annual expenses monthly — don’t let them hit you all at once

Rent in Dubai is usually paid annually or in two or four cheques, which means several months of the year you’re hit with large lump-sum payments that feel like they come from nowhere. The same applies to car insurance renewal, vehicle registration, school fees, annual flight home and holiday deposits.

Take the total of your large annual expenses, divide by twelve, and set that amount aside every month into a separate pot — some people label it ‘big bills’ inside a multi-account setup. When January arrives and you need to pay rent, the money is already sitting there rather than requiring a panicked scramble or a debt. It sounds almost too simple but it’s one of the most effective structural changes people make to their finances in Dubai.

11. Track where your money actually goes — even for just one month

Most people who feel like they can’t save have a rough idea of their biggest expenses but no clear picture of the small ones. One month of genuinely logging every transaction — YNAB, a simple Excel sheet, even a notes app — almost always produces a surprise. A subscription forgotten. Petrol higher than expected. Spontaneous purchases that individually seem small but collectively account for thousands.

You don’t need to track forever. Even a single month of honest tracking gives you a baseline that makes every subsequent budgeting conversation with yourself more productive because you’re working with real data rather than rough estimates.

Related : Top 10 Tips to Save Money on Dubai Rent — Ultimate Guide.

12. Build an emergency fund before you invest

Three to six months of living expenses in a liquid, accessible account — not in stocks, not in crypto, not in a product with a lock-up period. Just sitting in a high-yield savings account earning interest and available within 24 hours if needed.

In a country where employment visas are tied to job status, an emergency fund isn’t just financial prudence — it’s specifically relevant to the UAE context. Losing a job here starts a visa grace period clock alongside the financial pressure. Having three months of expenses available means you can job search properly, pay ILOE paperwork fees, and make considered decisions rather than desperate ones. Build this first, before any other investment.

13. Invest surplus in low-cost index funds — stop leaving money idle

Once the emergency fund is in place and the monthly savings habit is running, idle cash in a current account loses real value every year to inflation. UAE residents have several accessible, low-friction options for investing small amounts regularly.

Sarwa is a UAE-regulated robo-advisor that invests in diversified ETF portfolios from AED 100 per month. Interactive Brokers (IBKR) gives access to a broader range of ETFs including QQQM and S&P 500 trackers at low commission. Neither requires financial expertise to start — the principle is simple: invest a fixed amount every month, in a diversified low-cost fund, and leave it alone. The compounding effect across five to ten years on even modest monthly contributions is significant.

14. Stop renting or buying to impress people you don’t particularly like

This one comes up in almost every honest conversation about money in Dubai. A significant portion of lifestyle inflation here is driven by what people perceive others expect of them — the car upgrade, the Marina apartment, the weekend brunch at the right venue. Much of it is invisible pressure rather than genuine preference.

A practical test: if you stripped away what you think other people expect, would you make the same choices? The residents who’ve built genuine savings in Dubai almost unanimously describe a point where they stopped optimising for the appearance of a lifestyle and started optimising for actual financial freedom. The two often look very different from the outside, and the gap between them is where savings live.

15. Find a secondary income stream — even a small one

‘Don’t let your job be your only source of income’ is among the most upvoted financial comments in every Dubai expat thread, and for good reason. A single salary makes you exposed — to redundancy, to visa cancellation, to a market that moves faster than most people expect.

A side income doesn’t have to be large to matter. Freelance work in your field, tutoring, reselling, a content channel, consulting on weekends — AED 1,500 to 3,000 a month in additional income can be the difference between saving nothing and saving a meaningful amount, particularly for people on mid-range salaries where the margin is tight. Start small and treat it as income that goes directly to savings rather than to lifestyle. The habit is more valuable than the initial amount.

The Honest Version

None of this is complicated. Most of it is just about building the structural habits that prevent the small, daily version of yourself from spending what the thoughtful, longer-term version of yourself wants to save. Auto-transfer. Separate account. Cook at home. Pay the card weekly. Budget for the big bills monthly.

The Dubai context makes it slightly harder than elsewhere because the lifestyle pressure is real and the convenience of spending is extraordinary. But the residents who’ve built real savings here aren’t earning dramatically more than everyone else — they’ve mostly just stopped doing the expensive things that don’t actually make them happier and put that money somewhere it compounds instead.