Will Etihad Rail Raise Property Values Near You : A realistic look at where transit-driven property gains are plausible, and where a station nearby is mostly just a good headline.

Every time a country announces a new rail line, someone writes a headline about buying before prices rise. Etihad Rail’s passenger launch has produced a fair share of these, and the underlying logic isn’t baseless: there’s genuine, measured evidence from the UAE’s own transport history that proximity to rail can lift property values. The problem is that most of the coverage built on that logic doesn’t look closely at the actual stations being opened, what’s legally ownable by a foreign investor in each emirate, or how different an intercity train running six services a day is from an urban metro running every few minutes.

Note : This article is for informational purposes only and does not constitute financial or legal advice. Always conduct your own due diligence and consult a licensed real estate broker and, where appropriate, a qualified legal adviser before making any investment decision.

Quick take: the case, station by station

Will Etihad Rail Raise Property Values Near You :The Full Picture

The table below maps every announced station against two questions: what kind of place it actually is, and whether there’s an established residential property market nearby worth paying attention to. A station opening doesn’t automatically mean housing prices will move — several stops on this network sit in industrial zones or towns with no meaningful residential market.

Always verify with a licensed broker and the relevant land authority before drawing any conclusions from this overview.

| Station | Emirate | What’s here | Property market reality |

|---|---|---|---|

| Mohamed bin Zayed City | Abu Dhabi | Residential suburb, not a designated investment zone | No direct play at the station itself; nearby areas like Reem Island, Al Reef and Zayed City are worth watching |

| Jumeirah Golf Estates | Dubai | Established golf community with freehold residential options | Strongest structural case on the network — three transport layers converging on one site |

| Al Dhaid | Sharjah | Agricultural oasis town | No established residential investment market |

| University City | Sharjah | University cluster near Sharjah airport | Strong student rental demand in nearby Muwaileh; not a resale story |

| Al Sila | Abu Dhabi (Al Dhafra) | Industrial and border zone | No residential market |

| Al Dhannah | Abu Dhabi (Al Dhafra) | ADNOC operations hub | Industrial only; no residential market |

| Al Mirfa | Abu Dhabi (Al Dhafra) | Industrial coastal town | No residential market |

| Madinat Zayed | Abu Dhabi (Al Dhafra) | Regional service town | No residential market |

| Liwa | Abu Dhabi (Al Dhafra) | Desert oasis, largely agricultural | No residential market |

| Al Hilal (Fujairah) | Fujairah | East coast tourist area | Tourism and hospitality activity; not an established housing market |

What We Actually Know About Transport and Property Prices Here

The closest available comparison isn’t an overseas case study — it’s the Dubai Metro. CBRE’s 2023 Dubai Metro Report analysed more than 74,000 residential sales transactions and close to 112,000 rental contracts going back to the metro’s 2009 launch. The headline finding: homes within a 15-minute walk of a Red Line station saw average prices rise 26.7 percent between 2010 and 2022, against a citywide average of 24.1 percent — a real but fairly modest outperformance.

The more interesting detail is where that outperformance concentrated. Properties 10 to 15 minutes from a station, not the ones immediately outside it, gained the most, at 43.8 percent. Rents showed an even sharper split: citywide rents fell 4.1 percent between 2018 and 2022, while rents within 15 minutes of a station rose 5.7 percent over the same period.

An earlier academic study, published in the Journal of Transport and Land Use, dug into why proximity doesn’t translate evenly into value. For residential property specifically, researchers found the relationship is concave: prices very close to a station, within roughly half a kilometre, were actually lower, most likely down to noise and traffic, while the strongest premium, somewhere around 700 to 900 metres out, ran to about 13 percent.

Commercial property told a different story entirely. The effect there was positive at nearly every distance and peaked around 76 percent in that same 700-900 metre band, several multiples larger than the residential effect. If there’s one consistent finding worth carrying into the Etihad Rail conversation, it’s that retail and food-and-beverage space near a station tends to benefit more, and more reliably, than the homes around it.

Why Etihad Rail Isn’t Quite the Same Bet as the Metro

The Dubai Metro is an urban transit system with dozens of closely spaced stations and trains every few minutes. Etihad Rail is an intercity network with a handful of widely spaced hubs and, at launch, six daily return services on the Abu Dhabi-Fujairah route. That difference matters in a practical sense: the metro effect comes from converting an entire corridor into walkable, transit-served real estate, while an intercity station behaves more like a small airport — a single high-value node rather than a line of value running through a neighbourhood.

Where an uplift exists, it will cluster tightly around the station itself and around whatever feeder transport — buses, taxis, an existing metro interchange — actually carries people the rest of the way.

That last-mile problem is not theoretical. Residents of Saadiyat Island, Palm Jumeirah or Arabian Ranches will still have to begin their journey in a car or taxi, and that arriving passengers must complete the final leg once they reach their destination — making the net time saving less clear-cut than the headline journey time suggests.

Etihad Rail is aware of it: the company has integrated the Abu Dhabi station into the Hafilat bus network, runs a Dh10 shuttle to Reem Mall and Adnec, and has placed rental car desks and e-hailing points at the Fujairah terminal. But a station with weak last-mile connectivity is a meaningfully weaker real estate catalyst than one already plugged into a metro, bus and highway interchange — which is exactly why the next section starts with the one station that already has all of that.

Jumeirah Golf Estates, Dubai: The One Genuine Property Story So Far

Jumeirah Golf Estates already has a working Dubai Metro Red Line station. The Etihad Rail terminal is being built directly across from it with a connecting footbridge, and a planned Dh34 billion Gold Line is set to terminate at the same site, alongside direct access to Sheikh Mohammed Bin Zayed Road. That’s three confirmed transport layers converging on a single site — close to the textbook description of the kind of node that produced the largest gains in Dubai’s own metro data.

What makes the JGE case structurally different from every other station on this list is who controls the land the terminal is being built on. The Etihad Rail station sits inside Wasl’s The Next Chapter, a 4.68 million square metre masterplan expansion currently underway.

The development adds 12,345 new residential units across six districts — 780 villas, 62 ultra-luxury hilltop mansions, 97 branded residences, 752 estate homes and 10,654 apartments — alongside a 5,000-seat tennis stadium, a Mandarin Oriental hotel and 48,000 square metres of retail and dining space. Wasl isn’t marketing proximity to the station; it’s marketing direct access to a terminal on its own land. That distinction matters: in a district reaching rail for the first time, a new station changes the fundamental accessibility proposition. At JGE, the station is already embedded in the developer’s pricing architecture.

Nearby established communities, Al Furjan, Dubai Investment Park, Dubai Production City and Green Community, sit within range of the same interchange, arguably the more accessible version of the opportunity for buyers who can’t stretch to JGE villa prices.

Two caveats are worth holding onto. The Gold Line and the high-speed Abu Dhabi-Dubai connection are both years away, so part of this thesis is genuinely forward-looking. And even the strongest version of the Dubai Metro evidence shows outperformance in low single-digit percentage points per year — not the kind of overnight repricing that some coverage implies. This is a multi-year structural tailwind, not a trading opportunity.

Mohamed bin Zayed City, Abu Dhabi: Why the Station Itself Won’t Move Prices

Mohamed bin Zayed City is not one of Abu Dhabi’s designated freehold investment zones — the areas, including Yas Island, Saadiyat Island, Al Reem Island, Al Maryah Island, Al Raha Beach, Al Reef and Masdar City, where non-GCC foreigners are legally permitted to hold full ownership. Roughly 40 percent of Abu Dhabi’s residential land sits outside those zones, reserved for UAE nationals and long-term leasehold arrangements, and MBZ City falls into that category. Whatever happens to values immediately around the station, most outside investors simply can’t participate in it directly.

The more realistic story is the ripple effect onto the freehold areas the station actually connects to. Etihad Rail’s Dh10 shuttle links Mohamed bin Zayed City directly to Reem Mall on Al Reem Island, one of Abu Dhabi’s established freehold zones, alongside Adnoc’s headquarters and the Adnec exhibition centre.

Al Reef, the most affordable of the capital’s designated investment zones, sits a short distance away and has long been positioned as an entry point for first-time foreign buyers. And Zayed City, the planned district between Mohamed bin Zayed City and Abu Dhabi International Airport, is being built under Abu Dhabi’s Plan 2030 with integrated rail and metro connectivity designed in from the outset — making it worth watching as the most direct long-term beneficiary of this corridor, even though it isn’t generating headlines yet.

University City, Sharjah: A Student Housing Story, Not a Homeowner One

The Sharjah station serves the emirate’s main cluster of higher-education institutions, including the American University of Sharjah and the University of Sharjah, and sits close to Sharjah International Airport. The people travelling through it are overwhelmingly students, staff and visiting families rather than commuters house-hunting nearby.

Sharjah’s property law adds another layer that’s easy to overlook. Foreign ownership there is limited to specific designated zones — Aljada, Tilal City, Maryam Island and Masaar among the better-known ones — none of which sit directly adjacent to University City. The realistic beneficiary of improved rail access here is Muwaileh, the established student-housing district next to the university cluster, where rental demand is already strong and yields across Sharjah’s freehold market generally run between 6 and 10 percent. Better intercity transport doesn’t turn Muwaileh into a freehold zone, but it adds one more reason for institutions, landlords and families to value proximity to it — an effect that tends to show up in rental performance over time rather than in resale prices most foreign investors can act on directly.

Al Dhaid and the Al Dhafra Stations: A Logistics Story, Not a Residential One

Six of the stations on this network sit in places with no residential investment case at all, in the way that term is usually meant. Al Dhaid is a Sharjah oasis town built around agriculture, not a freehold zone or an emerging suburb. Al Sila, Al Dhannah, Al Mirfa, Madinat Zayed and Liwa — the five Al Dhafra region stations due in December — sit in Abu Dhabi’s western region around ADNOC’s major industrial and petrochemical operations. None of them appear on any current list of designated foreign-ownership zones.

What these stations more plausibly support is industrial and logistics real estate: warehousing, freight-adjacent commercial space and the kind of business infrastructure that follows reliable transport links between ports, refineries and the rest of the network. That’s a legitimate economic story, arguably a more durable one given the scale of ADNOC’s operations in the region, but it’s a commercial and industrial thesis, not a residential one.

The More Interesting Read: Commercial, Not Residential

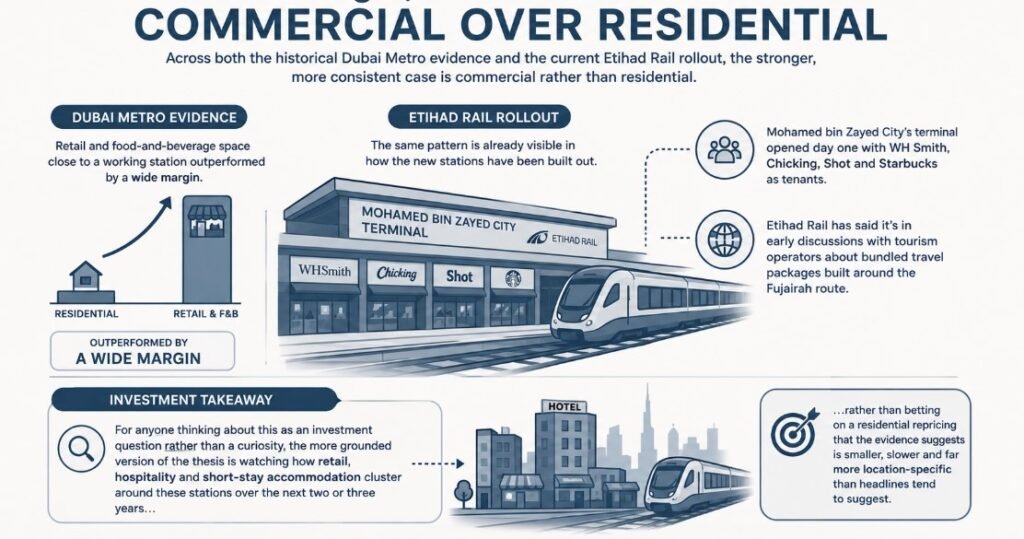

Across both the historical Dubai Metro evidence and the current Etihad Rail rollout, the stronger, more consistent case is commercial rather than residential. Retail and food-and-beverage space close to a working station outperformed by a wide margin in the metro data, and the same pattern is already visible in how the new stations have been built out. Mohamed bin Zayed City’s terminal opened day one with WH Smith, Chicking, Shot and Starbucks as tenants, and Etihad Rail has said it’s in early discussions with tourism operators about bundled travel packages built around the Fujairah route.

For anyone thinking about this as an investment question rather than a curiosity, the more grounded version of the thesis is watching how retail, hospitality and short-stay accommodation cluster around these stations over the next two or three years, rather than betting on a residential repricing that the evidence suggests is smaller, slower and far more location-specific than headlines tend to suggest.

A Short Checklist Before Acting on Any of This

- Confirm the area is actually inside a designated freehold or foreign-ownership zone for that specific emirate. ‘Near a station’ and ‘legally ownable by a foreigner’ are two separate questions, and the rules differ by emirate.

- Measure real walking time to the platform, not driving distance. The evidence consistently shows the effect concentrated within a 15-minute walk, not a 15-minute drive.

- Weigh last-mile connectivity — buses, taxis, an existing metro link — as heavily as the station itself. A station without it is a meaningfully weaker catalyst.

- Treat this as a multi-year thesis. The clearest UAE evidence available, from the Dubai Metro between 2010 and 2022, shows outperformance accumulating over more than a decade, not months.

- Speak to a licensed real estate broker and, where relevant, a lawyer familiar with that emirate’s specific ownership rules before committing capital. This article is informational and not financial or legal advice.

One station, Jumeirah Golf Estates, has a genuine, multi-layered transport case already backed by developer investment on land the developer controls. A couple of others offer plausible secondary effects on nearby freehold areas or specific niches like student housing. Several stations with no residential story at all sit in industrial towns and petrochemical hubs where the upside, if any, belongs to logistics and warehousing rather than apartments.

None of this is fixed. The Gold Line, the Abu Dhabi-Dubai high-speed link, and any feasibility decision on extending passenger services to additional emirates — including Ras Al Khaimah and the Northern Emirates — are still ahead. Stations that look purely industrial today, or freehold rules that currently exclude a given area, can shift as the network matures. Worth revisiting once the Dubai and Sharjah legs open in September.